What Types of Car Insurance Coverage Do I Really Need?

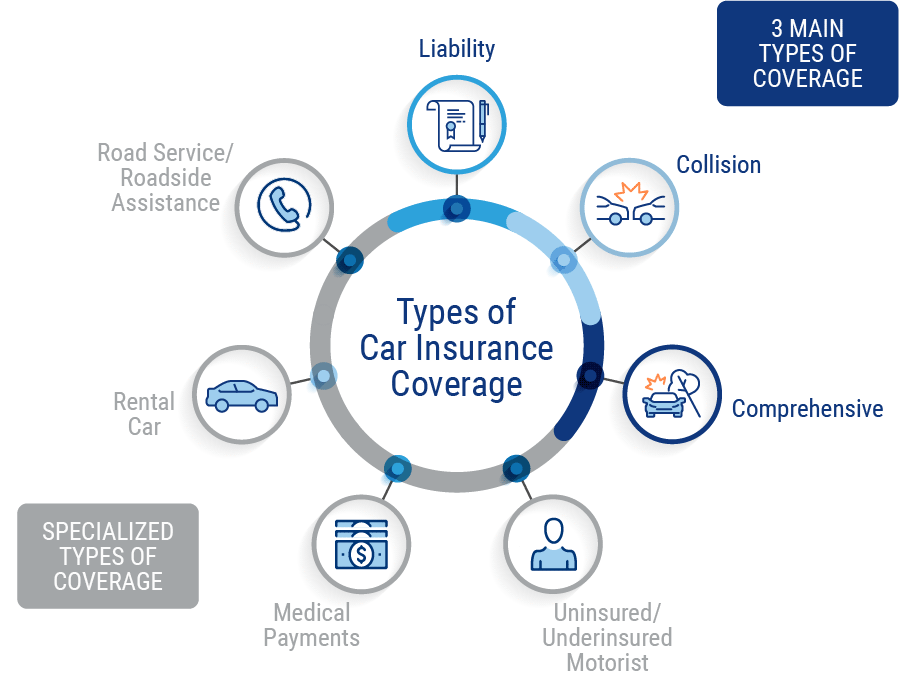

The type of car insurance you’ll need will depend on the type of car you drive and your budget for insurance. If you finance your Auto, your financing company will likely require you to buy full coverage on your car, which means you buy both collision and comprehensive coverage.

Since so much of your car insurance premiums are determined by your driving history, then the type of car insurance you buy will also partly depend on your driving record.

For example, if you’ve had multiple accidents in the last three years, you’ll be considered a high-risk driver and will pay much higher rates, no matter which coverage types you choose. But if you have a safe driving record with no violations or accidents, your rates will be much lower, which means you might be able to afford to add some extra coverage options.

How Much Does Car Insurance Cost?

The average cost of car insurance in the United States is around $1,300 a year, or about $110 a month. However, that number is the average cost across the entire country, meaning it takes into account rates in expensive states like Michigan and California along with rates in cheaper states like South Dakota and Missouri.

Car insurance rates are mainly based on:

- Age: Younger drivers under the age of 25 pay the highest rates, mainly because that age group gets into the largest number of accidents.

- Location: City drivers pay more than rural drivers due to the increased likelihood of having a claim (traffic jams, thefts, stop-and-go driving).

- Gender: Female drivers have lower rates than male drivers due to their better driving records.

- Driving history: Your own driving history plays a large role. If you’re a safe driver, you’ll have fairly low rates for your Auto type and location.

- Type of Auto : The more expensive the Auto , the more it will cost to insure because the insurance company will have to pay more money to replace it. Pickup trucks are among the most expensive vehicles to insure because they are involved in more accidents and can cause more damage.

- Current insurance: Some insurance companies require you to have a current policy in force before they will insure you. If you don’t have prior insurance or have a long lapse in coverage, your options will be more limited and you’ll likely pay higher rates.

- Credit score: Credit scoring may not stick around as it’s being reviewed by state legislatures as an insurance rating tool at the time of this writing. But most states still use it as a rating factor, with better credit scores leading to lower rates.

Who Is Included on My Car Insurance Policy?

When you buy a new car insurance policy, you’ll be asked to list all the drivers who should be on your policy. This typically includes anyone living in your household.

You’ll definitely want to include any Auto that is titled and could be driven. Car insurance primarily follows the car, not the driver. If you get pulled over by the police, they are looking to see if that vehicle is insured, not if the person driving the vehicle is on the policy or not. As far as insurance, the police only want to see if the vehicle is covered by an active insurance policy.

You can let anybody drive your Auto and they will be covered under your policy. But insurance companies want you to list anyone who has regular access to your Auto as a driver.

If you knowingly omit a driver, such as your teenage driver who just got their license because you know your rates will spike, you could be risking having your claim denied by the insurance company.

How Can I Get Car Insurance Discounts?

Most insurance companies offer more discounts on car insurance than any other type of insurance. Each company offers slightly different discounts, but some of the most common ones include:

- Multi-policy: Almost every insurance company offers a multi-policy discount, which knocks off 10% to 20% when you bundle your car insurance with a homeowners or renters policy.

- Multi-Auto : If you have more than one Auto on your policy, you’ll likely receive this discount, which makes each Auto in a household slightly less expensive to insure than it would be if it was the only car on the policy.

- Auto safety features: Most new Auto have advanced safety features, such as passive or active restraints and blind spot monitoring. Each Auto that has these is eligible for these discounts.

- Safe driving record: Insurance companies like to minimize risk, and having a safe driving record is a big indicator that you’re likely to keep your driving record clean. Companies typically look back between three and five years at your record, but this can be one of the larger discounts available.

- Good student discount: Having teen or early 20s drivers on your policy can have a dramatic impact on your rates. To help offset part of this, your child could receive a good student discount if they earned at least a B average last semester.

- Defensive driving course: Anyone is eligible for a defensive driving discount, but this can be particularly attractive to people who don’t qualify for a safe driving discount. Enroll and complete an approved online defensive driving course and receive a discount.

- Telematics: Not every insurer offers this, but enrolling in your company’s telematics program could save you extra money. Telematics is the program that tracks certain aspects of your driving for a period of months and gives you a discount based on how you drive.

There are usually many more discounts available, such as paying for your policy in full, enrolling in automatic payments, quoting well ahead of time, going paperless, etc. Be sure to talk with an independent insurance agent to find out which discounts you qualify for.

What to Watch Out for with Online Car Insurance Quotes

The main thing to watch out for when buying car insurance online is understanding what each coverage option is and resisting the temptation to just buy the cheapest possible insurance. There’s a difference between having an affordable, competitively priced car insurance policy with simply having the cheapest policy possible.

Oftentimes, the cheapest insurance will mean buying only the state minimum liability limits with no other types of coverage. Or having both collision and comprehensive coverage on your policy is expensive, you might be tempted to save money elsewhere, such as on your liability coverage.

Buying the state minimum liability limits can be very risky because it simply doesn’t cover you for much money if you’re responsible for an accident.

If you cause an accident and your insurance limits aren’t high enough to cover the other person’s injuries (or lawsuit costs if there’s a death involved), then you’ll be responsible for paying the rest of the money out of your own pocket. And if you don’t have that money laying around, your other assets could be taken, including your house, car, and a portion of your future earnings.